March 2, 2018 | by Laura Ross

Categories: Homeownership

A recent article published by point2homes.com examines how quickly homeowners can pay off their mortgages in the 50 biggest cities in North America. The conclusion was troubling.

Using the affordability ratio (also known as the median multiple)-- an indicator widely used to assess urban housing affordability--they found that only a small number of cities listed in the top 50 were deemed affordable, with 32 actually seen as seriously or severely unaffordable.

What is the affordability ratio?

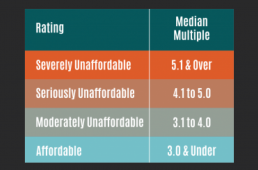

The affordability ratio calculates how affordable it is to live in an area by taking the median home price and dividing it by the median income. In other words, if a home buyer was to use their full annual salary to pay off their mortgage, the ratio calculates how many years it would take to do so.

A ratio of 3.0 and under is considered affordable, 3.1 to 4.0 is considered moderately unaffordable, 4.1 to 5.0 is considered seriously unaffordable and 5.1 and over is considered severely unaffordable.

There were several Texas cities included in the study. Both Dallas and Austin ranked in the top 25 at No. 17 (Dallas) and No. 24 (Austin). With affordability ratios over 5, both are considered severely unaffordable. San Antonio (No. 28) and Houston (No. 29) have ratios of 4.7 and 4.5, deeming them seriously unaffordable. Fort Worth (No. 33) and El Paso (No. 43) rounded out the Texas cities on the list. While their affordability ratios were lower at 4.0 and 3.3 respectively, they are still considered moderately unaffordable using the affordability ratio indicator.

Why is there such a gap in housing affordability?

The affordability gap can be attributed to several factors, including rising home prices and the decline of entry-level homes in urban areas. Click here and here to read previous blog posts on these topics. Rising home prices can benefit existing homeowners, but make it difficult for first-time buyers to find homes in their price range.

How can TSAHC help bridge that gap for first time home buyers?

TSAHC offers both down payment assistance and mortgage tax credits to first time home buyers. When using the down payment assistance (DPA) program, not only do home buyers receive a low interest fixed rate mortgage, but they also receive a grant of up to 5% of the mortgage amount that they can put towards their down payment and/or closing costs.

TSAHC also offers a mortgage interest tax credit, known as a Mortgage Credit Certificate (MCC), specifically for first-time buyers. With an MCC, home owners can claim a credit on their income taxes of up to $2,000 every year for the life of their home loan. First-time buyers can use TSAHC’s DPA and MCC programs together. For more information on TSAHC’s programs and to see if you qualify, click here.

On the House blog posts are meant to provide general information on various housing-related issues, research and programs. We are not liable for any errors or inaccuracies in the information provided by blog sources. Furthermore, this blog is not legal advice and should not be used as a substitute for legal advice from a licensed professional attorney.

I purchased a home and qualified for Tsahc. Nov 3, 2017

My lender first said I qualified for MCC before closing but did not include the MCC tax credit information or account number in my loan documents. I didn’t catch this until after I closed and when I was filing my taxes for 2017. When I asked for the MCC certificate he said I didn’t qualify. He could not explain why and has since ignored my communicatikns.

What is needed to qualify?

How does someone qualify?

Why did I not qualify?

TSAHC reviews all blog comments before they are posted to ensure a positive experience for our online community. Off-topic comments; hostile, derogatory or deliberately insulting comments; and comments specifically promoting goods and services will not be posted.

Approved comments will be published in their entirety. Personal information will not be removed unless it pertains to someone other than the person submitting the comment. For more information, please see our Comment Posting Guidelines.

To remove a previously submitted and published comment, please contact Anna Orendain at [email protected].

If you have a question regarding any of TSAHC's programs, please contact us.

Hi Bradford, Information on the MCC program can be found here: https://www.tsahc.org/homebuyers-renters/mortgage-credit-certificates. Its hard to know exactly why your lender determined that you didn’t qualify for the program, though income is calculated differently when determining eligibility for the DPA and MCC program which might be the reason.